Intro

Master Money Management Strategies in 2025 with SMART goals. Build wealth and achieve financial freedom effectively with LoppZ.

Having a goal is important but more important is having a SMART goal. Whether you want to save for emergencies or retirement, pay off your debt, be financially independent or want to work on other money objectives, setting S.M.A.R.T financial goals is very important to achieving your desire.

In a world full of intentions, SMART goals are the separating bench line between you and a daydreamer.

But before we take you through all you need to know to set a SMART goal, go ahead and like, subscribe and turn on the notification button.

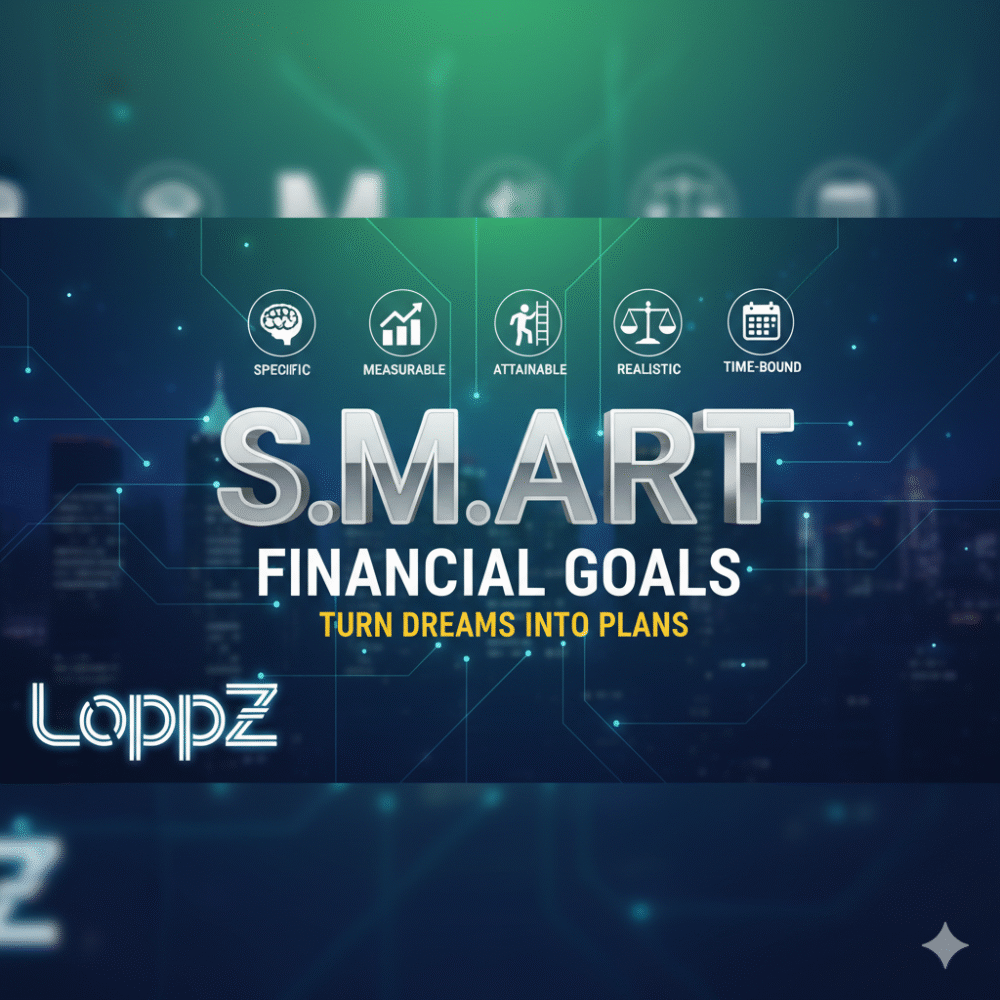

- Now, let’s show you how to turn your money objectives into strong powerful resolutions. , Briefly s.m.a.r.t means your goal should be:.

Intelligent. Target

Typical (so that you will become clear about what you are trying to achieve) measureable (numerical, to help you track progress) (so that you can get it real) to save it, college, college, emergency, retirement, or saving for any other financial goals.

Also, you should understand that setting financial goals is a vital first step toward achieving your vision for your future. But it’s easy to make the slip-up of setting excessively vague goals like “I want to make more money or save lots of money”.

This is where the SMART goal strategy comes in to make your goals easier to accomplish. To do this, you have to follow a few steps.

- 1. Make Your Goals Specific The first thing to do is shift away from “I.

Specific

want more money” to being specific about your target. This is necessary because without you being specific on the “what” and “why”, those goals are just mere daydreams that would eventually be given up.

- To develop a specific goal, you have two clear items. Firstly, you should know what you want and then how much of what you want.

For instance, if what you want is to save money; how much should be the quantifiable amount. This is an amount that can be counted; a definitive amount.

Secondly, you must state the reason for your goal, and why you’re going to achieve this goal. it’s important because it gives you a sense of purpose and vision without which you can’t achieve any worthwhile goal.

- When you give details like these to your financial goals, it will help you keep the focus on.

Measurable

- the prize. 2. Make Your Goals Measurable Quantifiable goals; goals you can put in figures, are simpler to keep track of because they are detailed.

Also, measurable goals can be broken into bits to help you make checks and balances along the way, to see if you’re making progress or not, which would require you to re-evaluate your goal.

For example, let’s say you’re looking to save $4,000 within a year, you can break it down to $1,000 every 3 months which means you have to save $334 per month.

- Who says you can’t further divide it to a daily target of about $12 per day? Now you see, it’s easier and simpler to track.

- You can now work toward your goal on a daily basis by the simple act of quantifying it. 3..

Attainable

Set For Yourself objectively Attainable Goals It is important to make your quantifiable goals attainable. Today’s world is filled with “higher intentions” which we are not against, but ensure that you make your goals specific enough to fit into your situation so you can plan to kick it into action.

Goals are not one size fits all. Ensure your goals are attainable for you. Again, let’s say your goal is to save $1,000 per month to pay down your debt or put separately for your summer holiday fund, but your monthly income statement says that you earn $1,200 per month.

When you put down $1,000 to this goal, what happens to the other expenses within the month? Is this amount feasible over the long term? Where will you get the funds? You have to ensure that what you set is attainable for the long run and will not cause you more issues.

- 4..

Realistic

Keep Your Goals Realistic When you set a realistic goal, you’re stating that there’s a reasonable percentage chance that you can accomplish it. To do this, you can task yourself to commit as much as you CAN to your goal.

The good thing is that only you can tell if your goal is realistic or not. Don’t let others set your goals for you! When you figure that out, it would help put down the actions you need to attain this goal.

Maybe putting aside $1,000 at the end of every month is realistic for you if you increase your sources of income or when you shrink your budget.

One way to help you set realistic goals is to scale your goals to your unique situation instead of following others, this way you can solve the issue of overshooting or undershooting.

So instead of putting aside $1,000 every month immediately, you could start by saving $500, and slowly increase it every couple of months until you’ve reached your desired amount.

- The objective is to meet a goal, not to starve yourself to death!.

Time

5. Give Time to Your Goals Ok, so by now, you know what makes your goal specific, how to measure your goal, you have set aside plans on how you will achieve it and you can also check if it’s realistic.

Now it’s time to put time into the goal because when you tell yourself “I’ll meet my goal to unsettle my college debt ‘someday’”, you probably will never meet that goal because it’s a never-ending path that leads to nowhere.

To help you set better goals at this point, ask yourself, does my goal have a really specific timeframe? Will the timeframe keep me focused? Is my goal SMART? Subsequently, when you want to set goals to save a down payment, you can say “I will put $15,000 aside every year for the next 3 years for a down payment on my future home.

I will achieve this by putting $417 into a savings account every month.” Or for a goal to help you clear a credit card debt, you can say “I will pay off my $2,500 credit card debt in 9 months by saving $278 every month toward it.

- I will accomplish this by cutting down my entertainment budget and not using my card during this period”. These kinds of goals are typically SMART.

Remember, SMART goals must prove what’s realistic for your unique situation. There might be little hiccups along the way, but don’t be afraid to re-evaluate and adjust as appropriate and then get back to achieving it as soon as you are comfortable.